It’s late in the second half, and your favorite team is comfortably ahead. The statistics look great—they’ve dominated possession, avoided mistakes, and executed the game plan exactly as designed. Everything points toward a win.

But suddenly the momentum shifts. The game starts to feel different. What once looked like a sure victory now feels uncertain. The scoreboard shows where things stand—but it no longer tells you how the game will end.

A similar disconnect shows up in investing all the time. One reason this disconnect shows up is that many strategies are built by looking backward. Past returns. Historical averages and historical Volatility metrics. They feel concrete and reassuring because you can measure them. But ask yourself: When has the future ever behaved exactly like the past?

Real investing doesn’t show up as a historical average. It shows up as uncertainty. As stretches of discomfort. As moments when even a “good” long-term strategy can feel very wrong in the short term. And that’s where you may struggle. Not because the strategy was flawed on paper, but because it demanded more patience, more emotional endurance, or more risk tolerance than you expected.

You don’t need to understand statistics or complex models to grasp the core idea. We can all agree that the future is always uncertain. The question isn’t whether uncertainty exists. The question is whether your investment process acknowledges it or quietly ignores it.

The P-PRO process starts from that reality. It’s about building a disciplined, rules-based approach that respects uncertainty, manages risk along the way, and aligns the strategy with your goals, your time horizon, and your ability to stay invested when markets inevitably test your resolve.

In the sections ahead, we’ll talk through why some advisors’ and most buy-and-hold strategies can fail in practice. We will discuss how growth, risk, and time interact in the real world, and how the P-PRO process is designed to help investors navigate all three calmly, deliberately, and with greater confidence.

Why Traditional Buy-and-Hold Often Breaks Down in Practice

On paper, buy-and-hold sounds almost unassailable. Stay invested. Ignore the noise. Let compounding work for you. The market “always comes back higher”. And it is true that if you can hold through market downturns, history has shown that you’ll be rewarded over time.

But there’s a quiet assumption buried inside that logic, and it is one that deserves more scrutiny than it usually gets. It assumes investors can ride all the normal swings of the market with the same emotional ambivalence.

In theory, discipline is simple. But in real life, drawdowns and volatility don’t arrive as those neat percentages on your spreadsheet or Fact Sheets. They may arrive as your company is doing a reorganization. As headlines about the government debt or politics feel alarming. As a retirement date that suddenly feels closer than it did before. The long-term goals are still there, but the short-term realities are screaming. When losses pile up, and uncertainty stretches on, the question shifts from “Is this strategy sound?” to “Can I keep doing this?”

When investing theory slams into reality, three things start to happen:

- First, a pull to “do something” starts to develop because the experience becomes too uncomfortable. Too stressful. Too disconnected from what you thought you signed up for.

- You become anxious as you seek more clarity, but it never quite arrives. Your reflexive brain pushes your logical, analytical abilities aside. Emotions take over, yet many times we do not realize it at the time.

- You start a cycle by selling a small amount, enough to feel like you have “done something”. Even if you do not sell any more, the cycle continues due to the hesitation that can occur as markets recover. When it starts to head back up without you, your confidence erodes and regret further replaces discipline.

Inconsistent experience is the real enemy. A strategy that delivers strong long-term results but does so through deep, unpredictable swings may look fine in hindsight, but it can still fail the investor living through it. Over time, that mismatch undermines trust, increases the likelihood of reactive decisions, and turns volatility from a temporary challenge into a permanent problem.

Buy-and-hold doesn’t break down because investors are irrational or impatient. It breaks down because people are human. And any investment process that ignores how investors actually experience risk over time is asking for discomfort.

The Three Forces Every Investment Strategy Must Balance

Every investment strategy wrestles with the same three forces: growth, risk, and time. Try to minimize or favor one, and another one eventually pushes back. The challenge isn’t choosing which one matters most. It’s understanding how they interact and where the tradeoffs really live.

Growth

It’s the part you want more of. Higher expected returns mean more freedom and more security. But, as with the other two, there is a cost. The cost of growth is usually paid with higher volatility of account values, or by experiencing more times when you think you made the wrong decision. The faster you try to grow, the more uneven the ride tends to become. This isn’t just a statistical concept. It’s something you must live through.

Risk

On paper, risk is measured mathematically, in things like volatility, drawdowns, and Sharpe ratios. Those metrics matter, but they only tell part of the story. Risk is also behavioral. It’s the chance that the costs of fear, doubt, or fatigue cause you to abandon a plan at the worst possible time. A strategy may be “optimal” in theory, but if it regularly pushes you past your emotional breaking point, what does it matter?

Time

Time is usually treated as an abstract input, a 10- or 20-year goal. But while goals like retirement can be generic, time isn’t. It’s personal. It’s tied to your specific cash flows, your transitions, the ebb and flows of your life’s journey that spring up before you reach your goals. You may have 3- or 5-year secondary goals. Furthermore, a strategy that works beautifully for one goal can be completely wrong for another, even for the same investor.

Problems arise when one of these forces is optimized in isolation. Maximize growth, and volatility may become intolerable. Minimizing short-term risk and long-term progress may fall short. Stretch time assumptions too far, and the plan becomes fragile when reality intervenes. What looks efficient on a spreadsheet can turn fragile in real life.

The most resilient investment strategies don’t chase a single variable. They recognize that growth, risk, and time are inseparable, and that balance is what allows you to stay committed when markets behave in ways no one can predict.

Why Investment Management Is Deeply Personal

It’s tempting to believe that your best friend, who is the same age and shares similar retirement goals, maybe even thinks about risk the same way, should have an investment strategy like yours. But that would be a wrong assumption. We may hope for the same long-term goals and go through the same bear market together, but we don’t experience risk, uncertainty, or loss the same way..

The reason is because our emotions are often triggered by a collection of our prior experiences. It’s impossible for everybody to have all the same life experiences, so two people can easily respond differently to the same current event.

Since investment management is deeply personal, we need to:

- Design strategies not just on intelligence or analytics, but on their probability to match our emotional responses.

- Not become enamored with investing “rules of thumb”. They can be a starting point, but strategies need to be tweaked and aligned with your specific situation.

- Understand that uncertainty will always exist. How comfortable can you be with being uncomfortable?

What Led to the Porter Performance Risk Optimized (P-PRO) Investment Process?

Much of the investment world has been anchored to a simple idea. Maximize return. Find the highest expected growth rate. And on the surface, that sounds logical. Who wouldn’t want the highest return? Aren’t we always trying to grow our money for something?

But here’s the problem. “Maximum return” thinking quietly assumes that the path doesn’t matter. By using a specific historical path (past returns, past drawdowns, etc.), you are only projecting history forward, attempting to reach a desired point in the future. But the future is never more than a range of possible outcomes. And a historical path of an investment or a strategy, one that had “great returns”, is just the one path that occurred, from a range of possible paths that could have occurred from an earlier point in time.

What led to the development of the Porter Performance Risk Optimized (P-PRO) Investment Process was a growing recognition that return alone is an incomplete metric. What matters far more is the range of possible return outcomes you could realistically experience, and the probability of each occurring over timeframes relevant to you.

Instead of only asking, “What could this strategy earn?” when looking at options, we began asking more grounded questions:

- What gives you a higher probability of achieving what you need and want?

- What are your chances of losing money?

- What is the most likely outcome?

- Is this strategy meaningfully better than something else? An Index?

When you shift from maximizing return to understanding probabilities, the conversation changes. It becomes less about chasing upside and more about managing tradeoffs. Less about forecasting and more about preparation. You can see not just the potential reward, but the potential experience. That’s where P-PRO connects volatility tolerance with real decision-making capacity.

By framing strategies in terms of probable ranges rather than single-point expectations, P-PRO helps align the portfolio with what you can reasonably endure. Not what sounds good in a planning meeting—but what holds up during real uncertainty.

And perhaps most importantly, it redefines success.

Success is not perfection. It’s sustainability. It’s building a strategy that can navigate inevitable volatility without forcing reactive decisions that derail your long-term goals. Sustainability, or staying in the game, is best achieved by consistency. Over the decades of working with individuals, we’ve found the investors who succeed aren’t the ones who chase a market-beating return every year. They’re the ones who have average or slightly above average returns, for above average lengths of time.

The P-PRO Investment Process: A Structured, Rules-Based Approach

Over time, it became clear that many traditional allocation models, while still useful, weren’t enough. A static mix of stocks and bonds, rebalanced periodically, assumes markets behave in relatively stable patterns. It assumes correlations stay somewhat constant. It assumes volatility is tolerable. And it assumes investors will remain disciplined no matter what.

Porter Investments moved beyond traditional allocation models because we needed something more durable. Uncertainty is not just a rare disruption; it is a constant presence. Instead of relying on static allocations and long-term averages alone, the P-PRO Investment Process is built around hard-coded rules, instills the discipline to follow them, and the repeatability of them to sustain the portfolio. Rules matter because they remove ambiguity at those very moments where ambiguity feels overwhelming.

A structured, rules-based investment approach does 3 things for you:

- It minimizes emotional excesses. We will always have emotions, but when markets are rising, rules help prevent excessive risk-taking driven by optimism. When markets are falling, rules help prevent emotionally driven exits rooted in fear. They create predefined action steps so that choices aren’t made in the heat of the moment.

- It creates repeatability. A process that works only when conditions are favorable is more of a preference than a process. P-PRO is built to operate consistently across different environments. Not perfectly. Not flawlessly. But predictably.

- It creates emotional guardrails. It limits our ability to dictate portfolio changes. That stability creates space for better long-term outcomes.

Portfolios designed for consistency aim to smooth the investor’s experience. We cannot eliminate volatility entirely, but we can manage it thoughtfully. Again, the goal isn’t to outperform in every environment. It’s to avoid extreme swings that make the strategy difficult to stick with.

In the end, structure isn’t about rigidity. It’s about resilience. And resilience is what allows accounts to compound and long-term plans to survive real-world markets.

Using Data and Probability to Align Strategy with Goals

If investing is about balancing growth, risk, and time, then data helps us understand how those forces have behaved historically, and probability helps us frame how they might behave in the future. Not with certainty, but with informed expectations.

Analytics and statistical modeling aren’t used to forecast exact returns. They help in gaining insight into questions such as: How could a strategy possibly respond to different market environments, given its history? How deep can drawdowns realistically be, not just how deep they were in the past?

This is where tools like Monte Carlo simulations become valuable. Rather than assuming one straight-line return path, Monte Carlo modeling runs thousands of potential scenarios based on historical relationships, volatility patterns, and return distributions. The result isn’t a single projection. It’s a spectrum of possible futures.

This allows us to reframe the conversations with you from “This is what this investment has historically earned” to “This is what the most likely and least likely return outcomes could be”. Seeking a single point in the future, based on a gut feeling or hope, can lead to disappointment from unmet expectations.

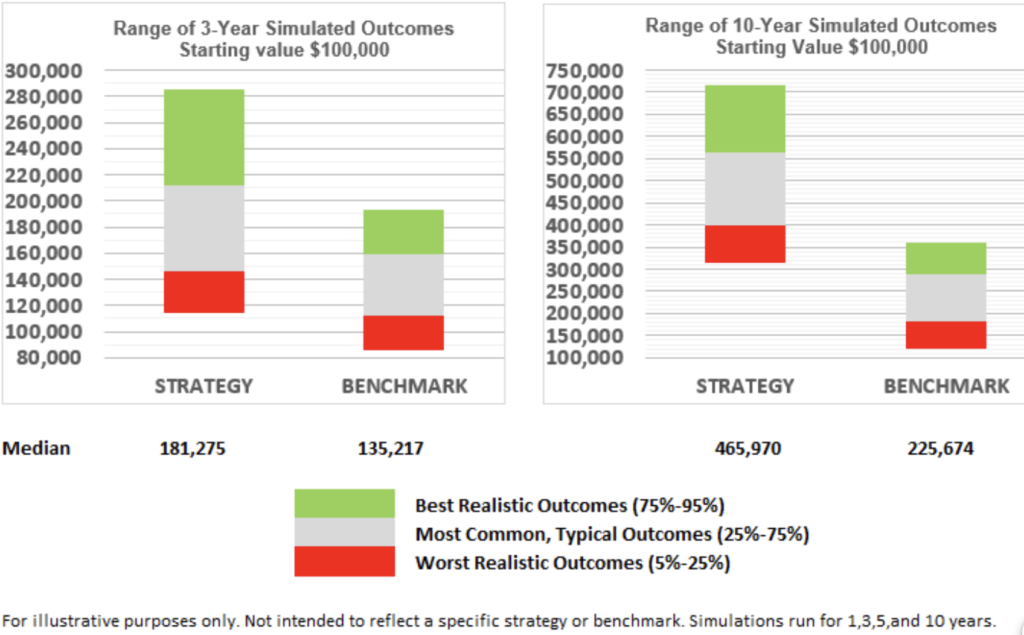

There is nothing wrong with optimism, but when you evaluate strategies based on likelihood rather than optimism, decisions become more durable. Your expectations are better aligned with what the real world can throw your way. You can quickly see and compare the realistic, but worst possible outcomes, that could sidetrack you. The following chart is a small example of what the process can reveal:

You are quickly able to compare the most likely outcomes of your investment strategy by looking at the relative position of the gray areas on the chart. But more importantly, you can see the relative likelihood of not achieving a goal within a meaningful timeframe. And you can now have a reasonable level of confidence (5%-95%) in most of the potential return outcomes a strategy could achieve. But most importantly, you will have more confidence in a strategy that optimizes the balance of your growth needs, your volatility capacity, and your time requirements.

You see not just the upside potential, but the risk, in a way that relates to you. It is not just some “risk score” derived from a questionnaire. It allows you to evaluate tradeoffs before living through them.

Managing Volatility to Improve Real-World Results

Volatility is often dismissed as background noise—an unavoidable feature of pursuing higher gains. Yet it can be much more than a nuisance.

A loss changes the math. Recovering always requires a larger percentage gain just to get back to even. Volatility is a fact of life, but spending more time than necessary recovering will slowly chip away at your long-term results.

You either manage volatility or it manages you.

How P-PRO Fits Within a Broader Financial Plan

P-PRO not only aligns your portfolio with longer-term retirement goals, but also with more intermediate goals and milestones. Each objective carries its own timeline and its own tolerance for variability. A single, generic allocation rarely accounts for those differences.

The P-PRO process is designed to coordinate growth expectations with actual spending horizons. If funds are needed in five years, the strategy must reflect that reality. If assets are intended to compound for decades, they can be positioned differently. The key is to match the probability of outcomes with when capital is expected to be used.

This alignment becomes especially important once cash flow enters the picture. Portfolios supporting withdrawals must consider sequence risk, which is the order in which gains and losses occur. A sharp decline early in a withdrawal phase can have lasting consequences. By incorporating volatility management and probability analysis, P-PRO helps structure portfolios to better sustain real-world income needs.

Ultimately, investing is only one component of a larger financial architecture. Tax planning, estate considerations, insurance coverage, and spending behavior all interact with portfolio decisions. A disciplined, probability-based approach ensures those moving pieces remain coordinated.

When investments are integrated thoughtfully into an overall plan, they become more than vehicles for return—they become tools that support stability, flexibility, and long-term clarity.

P-PRO Investment Process FAQs

1. How does P-PRO differ from traditional buy-and-hold strategies?

The P-PRO process differs from traditional buy-and-hold strategies by focusing on probability ranges and volatility management rather than assuming investors can simply endure all market cycles unchanged. Instead of remaining static, it uses structured rules to adapt within defined parameters while maintaining long-term discipline.

2. Is the P-PRO process designed for long-term investors?

Yes, the P-PRO process is designed for long-term investors, but it recognizes that long-term success depends on navigating short- and intermediate-term uncertainty effectively. It prioritizes sustainability so investors can remain committed over decades, not just in theory but in practice.

3. How does the process account for individual risk tolerance?

The process accounts for individual risk tolerance by aligning projected outcome ranges with each investor’s specific financial goals, time horizons, and decision-making capacity. Rather than relying solely on stated comfort levels or portfolio risk scores, it evaluates how different drawdown scenarios may realistically affect behavior.

4. What role do probabilities play in portfolio construction?

Probabilities play a central role in portfolio construction by helping evaluate the likelihood of various outcomes across relevant timeframes. Instead of chasing the highest possible return, the process weighs the chances of meeting specific objectives under different market conditions.

5. How does P-PRO help investors stay invested during market stress?

P-PRO helps investors stay invested during market stress by using predefined rules that reduce emotional decision-making and by managing volatility to create a steadier experience. By setting expectations around potential ranges in advance, it lowers the odds of reactionary shifts during downturns.

How We Help Investors Apply the P-PRO Process with Confidence

The P-PRO process may be built on rigorous analytics, but our role is to translate that complexity into clear, practical guidance you can understand and act on. That serves to not only align your portfolio with what you’re trying to accomplish, but with your true emotional capacity, regardless of what life throws your way over time.

If you’re curious how the P-PRO approach may confidently align your return, risk, and time objectives with your true comfort level, you can schedule a brief conversation with us.

Bob Porter is the President of Porter Investments. Porter Investments is a fiduciary investment management firm based in Houston, Texas, helping self-directed and hybrid investors gain professional guidance and grow their portfolios with tactical strategies. Bob's prior work at Fidelity Investments allowed him the opportunity to advise and study a diverse group of investors.

- Bob Porter

- Bob Porter

- Bob Porter

- Bob Porter

- Bob Porter

- Bob Porter

- Bob Porter

- Bob Porter

- Bob Porter

- Bob Porter

- Bob Porter